When compared to a medium severity medium frequency risk, the operational risk capital requirement for a high severity very low frequency risk is likely to be:

For a given mean, which distribution would you prefer for frequency modeling where operational risk events are considered dependent, or in other words are seen as clustering together (as opposed to being independent)?

Which of the following is not one of the 'three pillars' specified in the Basel accord:

Which of the following are a CRO's responsibilities:

I. Statutory financial reporting

II. Reporting to the audit committee

III. Compliance with risk regulatory standards

IV. Operational risk

Which of the following statements are true:

I. Capital adequacy implies the ability of a firm to remain a going concern

II. Regulatory capital and economic capital are identical as they target the same objectives

III. The role of economic capital is to provide a buffer against expected losses

IV. Conservative estimates of economic capital are based upon a confidence level of 100%

Which of the following should be included when calculating the Gross Income indicator used to calculate operational risk capital under the basic indicator and standardized approaches underBasel II?

An error by a third party service provider results in a loss to a client that the bank has to make up. Such as loss would be categorized per Basel IIoperational risk categories as:

Under the ISDA MA, which of the following terms best describes the netting applied upon the bankruptcy of a party?

Which of the following statements are true:

I. The set of UoMs used for frequency and severity modeling should be identical

II. UoMs can be grouped together into larger combined UoMs using judgment based on the knowledge of the business

III. UoMs can be grouped together into combined UoMs using statistical techniques

IV. One may use separate sets of UoMs for frequency and severity modeling

Which of the following is not a tool available to financial institutions for managing credit risk:

The standalone economic capital estimates for the three business units of a bank are $100, $200 and $150 respectively. What is the combined economic capital for the bank, assuming the risks of the three business units are perfectly correlated?

There are three bonds in a diversified bond portfolio, whose default probabilities are independent of each other and equal to 1%, 2% and 3% respectively over a 1 year time horizon. Calculate the probability that none of the three bonds will default.

A financial institution is considering shedding a business unit to reduce its economic capital requirements. Which of the following is an appropriate measure of theresulting reduction in capital requirements?

An investor enters into a 5-year total return swap with Bank A, with the investor paying a fixed rate of 6% annually on a notional value of $100m to the bank and receiving thereturns of the S&P500 index with an identical notional value. The swap is reset monthly, ie the payments are exchanged monthly. On Jan 1 of the fourth year, after settling the last month's payments, the bank enters bankruptcy. What is the legal claim thatthe hedge fund has against the bank in the bankruptcy court?

When considering a request for a loan from a retail customer, which of the following factors is relevant for a bank to consider:

A corporate bond maturing in 1 year yields 8.5% per year,while a similar treasury bond yields 4%. What is the probability of default for the corporate bond assuming the recovery rate is zero?

Aderivative contract has a negative current replacement value. Which of the following statements is true about its loan equivalent value for credit risk calculations over a 2-year horizon?

Whichof the following statements are true in relation to Historical Simulation VaR?

I. Historical Simulation VaR assumes returns are normally distributed but have fat tails

II. It uses full revaluation, as opposed to delta or delta-gamma approximations

III. Acorrelation matrix is constructed using historical scenarios

IV. It particularly suits new products that may not have a long time series of historical data available

When modeling operational risk using separate distributions for loss frequency and loss severity, whichof the following is true?

Identify the correct sequence of events as it unfolded in the credit crisis beginning 2007:

I. Mortgage defaults increased

II. Collapse in prices of unrelated assets as banks tried to create liquidity

III. Banks refused to lend or transact with each other

IV. Asset prices for CDOs collapsed

Which of the following steps are required for computing the total loss distribution for a bank for operational risk once individual UoM level loss distributions have been computed from the underlhying frequency and severity curves:

I. Simulate number of losses based onthe frequency distribution

II. Simulate the dollar value of the losses from the severity distribution

III. Simulate random number from the copula used to model dependence between the UoMs

IV. Compute dependent losses from aggregate distribution curves

Which of the following statements are true?

I. Retail Risk Based Pricing involves using borrower specific data to arrive at both credit adjudication and pricing decisions

II. An integrated 'Risk Information Management Environment' includes two elements - people and processes

III. A Logical Data Model (LDM) lays down the relationships between data elements that an organization stores

IV. Reference Data and Metadata refer to the same thing

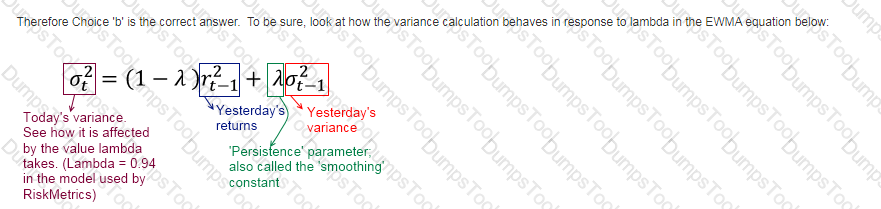

As the persistence parameter under EWMA is lowered, which of the following would be true:

Which of the following is not a limitation of the univariate Gaussian model to capture the codependence structure between risk factros used for VaR calculations?

Which of the beloware a way to classify risk governance structures:

A Reactive, Preventative and Active

B. Committee based, regulation based and board mandated

C. Top-down and Bottom-up

D. Active and Passive

Which of the following is true for the actuarial approach to credit risk modeling (CreditRisk+):

Which of the following statements is true

I. If no loss data is available, good quality scenarios can be used to model operational risk

II. Scenario data can be mixed with observed loss data for modeling severity and frequency estimates

III. Severity estimates should not be created by fitting models to scenario generated loss data points alone

IV. Scenario assessments should only be used as modifiers to ILD or ELD severity models.

TESTED 19 Jul 2026