Keitaro, age 42, and Ruth, age 52, are married and have two children - Maximo, age 20, and Hannah, age 16, both from Keitaro's previous marriage. In the event Keitaro dies, he would like to minimize taxes, provide for Ruth for the remainder of her life, and then after her death leave the residual to his children. What estate planning strategy should his financial planner recommend to help Keitaro achieve his goal?

A client’s portfolio target is 50% equities and 50% fixed income. After a strong equity market, the portfolio is now 68% equities. The client’s circumstances and objectives have not changed. What should the planner recommend?

What key question should be answered during the recommending strategies stage of the financial planning process?

Which asset is most likely to flow through a deceased person’s estate rather than pass automatically outside the estate?

John and Jerry's financial planner have recommended they review their budget. What is the primary purpose of the budget?

In order to increase the assets in Rebecca's retirement savings, her financial planner is considering making a number of recommendations. Prior to obtaining her current employment, she withdrew funds from her RRSP under the Lifelong Learning Plan to upgrade her skills. She has four annual installments remaining on her Lifelong Learning Plan withdrawal and a small amount of savings in a TFSA. Rebecca now works as a sales associate in a small clothing store that has a group RRSP program for all employees which matches employee contributions. Which recommendation provides the best long-term impact to grow her retirement savings?

A couple has stable employment, two dependants, and essential monthly expenses of $5,200. They have no emergency reserve. Which recommendation is most appropriate before increasing long-term investment contributions?

Jelena, age 32, is single and works as a partner in a law firm. She is meeting with her financial planner, May, as she would like to start investing. Her friend John talks about hot sectors in the stock markets and has recently brought up the cannabis sector. She has done some reading about this sector and is willing to experience large decline in her investments. Jelena also mentioned to May that she believes in high long-term returns. What conclusion can May draw based on their discussions about the stock market and Jelena's expectations?

What information is least important for Harry as a financial planner in his assessment for insurance coverage for his client with respect to estate planning purposes?

Gina plans to take a one-year leave of absence from her employer without pay. Gina has a TFSA invested in equity mutual funds which is currently below book value, an RRSP invested in cash, a Nova Scotia LIRA invested in GICs, and a line of credit. Assuming all have sufficient funds, which plan should Gina access to ensure she meets her goal of budget effectiveness during this time?

Jenny and Herman are looking for tax strategies that will help them better manage their marginal annual tax rates. Jenny is currently the primary income earner in the household. She has a large non-registered portfolio that holds only plain vanilla S & P 500 index funds. Jenny and Herman have a 14-year-old daughter, and they would also like to know what income-splitting opportunities exist. They’ve presented several ideas to their tax planner, Isaac, for review. Which of the following will likely result in tax attribution to Jenny?

A client wants to increase net worth by identifying spending reductions and increasing monthly surplus. Which document is most useful for this purpose?

A higher-income spouse contributes to a spousal RRSP for the lower-income spouse. The lower-income spouse withdraws the contribution amount the following year. What should the planner warn them about?

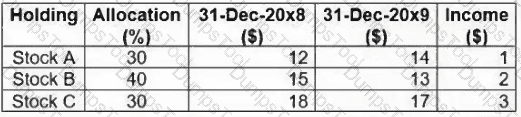

Consider the following information for a client's portfolio:

What is the annual rate of return for this portfolio?

Alexis has an index-linked GIC with an adjusted cost base of $20,500. The GIC was issued one year ago, has four years remaining to maturity and provides her with 60% participation in the gains of the S & P/TSX 60 Index, based on the level of the Index at maturity or at redemption prior to maturity. The GIC has a 2% fee if redeemed in the first two years. Alexis notices that the S & P/TSX 60 Index is up 25% and she would like to redeem her GIC. She asked her financial planner if she redeems her GIC, how much she would receive upon redemption. What will her financial planner tell her?

Keitaro wants his spouse to receive income from his assets for life after his death, but wants the remaining capital to pass to his children from a prior marriage after the spouse dies. Which strategy best fits this objective?

During the discovery process, Greyson and Jacob's financial planner identifies that the couple wants to protect their family from unexpected health events and premature death. Their financial planner coordinates a meeting with an insurance agent for the next steps. What should the insurance agent recommend?

Alexander and Irena, age 30 and 32 respectively, are married and have been working full-time for one year. They have a daughter, age 3, and are expecting their second child. They recently bought a home with a mortgage balance of $390,000 at 4% amortized over 25 years. Their financial planner is trying to determine their tolerance for risk. After completing the life-cycle analysis, how can their financial planner explain the stage in which the couple finds themselves and the risk tolerance associated with it?

A client believes that security prices quickly reflect public information and wants broad Canadian equity exposure with low cost and minimal manager discretion. What investment best matches this view?

Leena and Harry are married and hold RRSPs with a value exceeding $500,000. They are concerned about their final tax liability and want to cover the taxes after they have both died. What would their financial planner recommend them to implement in order for the couple to achieve the objective?

A client says she can emotionally tolerate a 30% portfolio decline, but she needs the money in 18 months for a home down payment and has no other savings. What should the planner conclude?

Samantha is meeting with a financial planner for the first time, seeking help with both investing and debt management. She's finding it hard to get ahead because she recently graduated with student debt, started a new career in her field, and is adding credit card debt each month. What recommendation should the financial planner propose?

Mark, a financial planner, is meeting his client Adam for the first time. From the conversation, Mark learned that Adam has some experience on trading stocks. Adam asked Mark to explain about efficient market theory that he overheard a colleague talking about a few days ago. How should Mark respond to Adam's question in simple terms?

Sarah Jones is an incorporated owner of a successful manufacturing company. She currently has a large month to month cash flow surplus. This is expected to continue until she retires in seven years. Her personal mortgage is up for renewal. She needs to borrow $50,000 so that she can replace a piece of equipment that is needed in the manufacturing process. She would like a solution that results in paying the lowest interest cost over the life of the loan. Which loan product should the financial planner recommend to Sarah? Assume monthly compounding for all products and no pre-payment options.

Tom has two children from a previous marriage. He has been paying $1,000 per month for spousal support and $1,500 per month for child support to his ex-wife. Recently, his ex-wife was awarded increased child support payments from Tom to cover unanticipated university expenses for one of the children. What should Tom's financial planner advise him about how this increased monthly payment may impact his finances?

Jackson, a wealth advisor, is helping Terry, a self-employed IT professional, determine his net income. The goal is to develop a budget and savings strategy for the year ahead Terry has provided the information below:

What is Terry’s net business income?

Evan meets with his financial planner to review his concerns around inflation and its impact on his TFSA investment portfolio. His financial planner researches the current holdings and recommends that he sells one of the portfolio’s equity funds. Which replacement option should the financial planner recommend to Evan?

Ivan has been relocated to a new office by his employer and is considering moving to a home closer to his new workplace. What is the minimum distance Ivan will have to move in order to qualify for the work-related moving expenses income tax deduction?

Rosa has just learned that her daughter Marissa, age 23, does not intend to return to university. She has been saving for her daughter's education since Marissa was 10 and is concerned there will be a significant tax liability. How should Rosa's financial planner advise her to utilize the funds when she redeems the RESP in order to offset the tax liability?

Ali wishes to retire in five years. His financial planner calculates that he needs to save an additional $40,000 to meet his retirement income objectives. What would Ali’s financial planner advise him to do in order to meet his retirement income objectives?

TESTED 04 Aug 2026