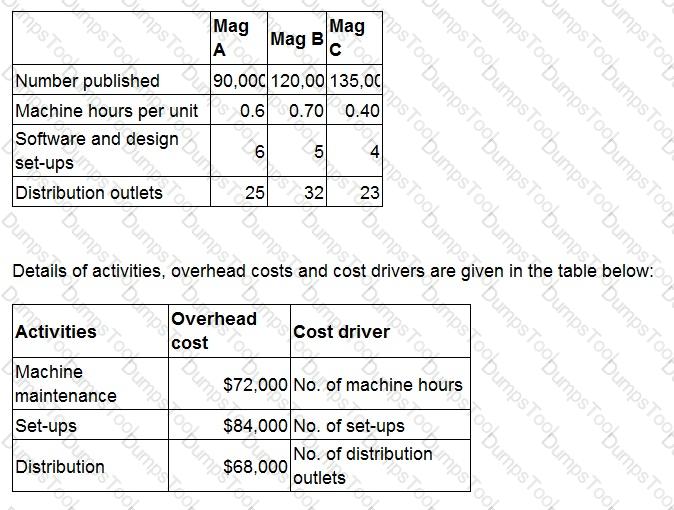

TDM edits, prints and publishes three magazines, Mag A, Mag B and Mag C. The company operates an activity-based costing system.

The following information has been obtained.

What is the overhead cost attributable for each Mag A publication?

Give your answer to the nearest whole cent.

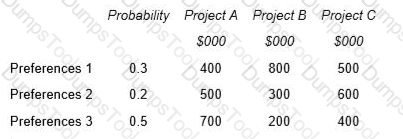

A company has to choose between three mutually exclusive projects. Market research has shown that customers could react to the projects in three different ways depending on their preferences. There is a 30% chance that customers will exhibit preferences 1, a 20% chance they will exhibit preferences 2 and a 50% chance they will exhibit preferences 3. The company uses expected value to make this type of decision.

The net present value of each of the possible outcomes is as follows:

A market research company believes it can provide perfect information about the preferences of customers in this market.

What is the maximum amount that should be paid for the information from the market research company?

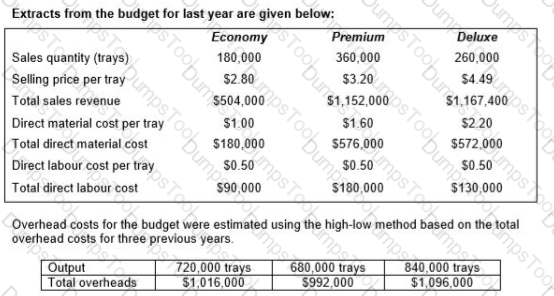

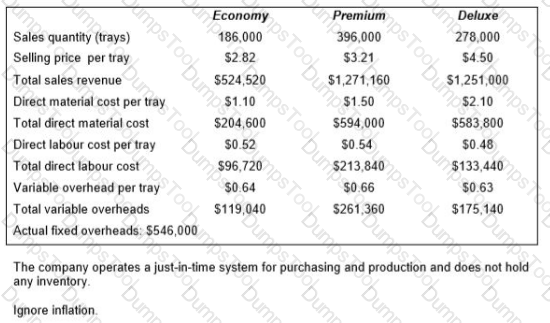

A company produces trays of pre-prepared meals that are sold to restaurants and food retailers. Three varieties of meals are sold: economy, premium and deluxe.

Calculate, for the original budget, the budgeted fixed overhead costs, the budgeted variable overhead cost per tray and the budgeted total overheads costs.

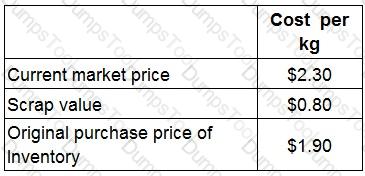

FGH used to manufacture components that required raw material Q.

Currently there are 80 kg of material Q in inventory.

The company has no use for the material in the foreseeable future and intends to sell it for scrap.

A potential new customer has asked for a price for a large order.

This order would require 100 kg of material Q.

The company management has decided to quote a price for this work on a relevant cost basis.

Details of costs for material Q are as follows:

What would be the relevant cost of Material Q to use in this order?

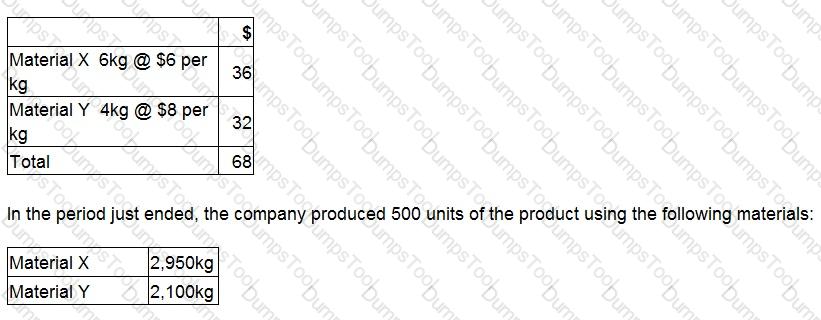

A company makes a product using two materials, X and Y.

The standard materials required for one unit of the product are:

What is the materials yield variance?

Give your answer as a whole number.

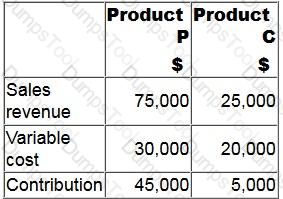

An entity manufactures two products.

The sales revenues of the products are in the constant mix of 3:1. Forecast data for next period are as follows:

The margin of safety for next period is $30,000 of sales revenue. Fixed costs are constant at all levels of output.

What is the forecast profit for next period?

Give your answer to the nearest whole number.

A company is considering the use of Material V in a special order.

The material is used regularly and a sufficient quantity of the material is in inventory.

It could also be sold, at just below the current market price, to a local competitor.

What is the relevant cost of Material V to be used in the special contract?

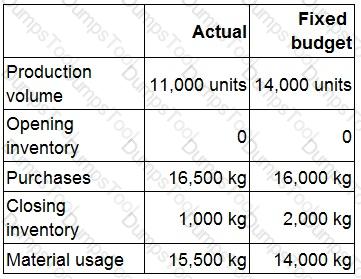

The performance of a production manager is assessed on efficient use of materials during the production process.

Actual data and data from the fixed budget for Month 4 are as follows:

What figures should be compared in order to assess the production manager's performance for Month 4?

A company uses an activity based costing system. The company manufactures three products, details of which are given below:

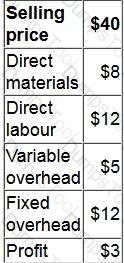

A company is considering whether to launch a new product. The selling price and costs for each unit of the product are shown in table below:

The fixed overhead cost is based on expected production of 2,000 units.

The company will only launch the product if it is expected to be profitable.

To which of the following is the decision to launch the product most sensitive?

In a manufacturing company, breakeven occurs at which TWO of the following?

Which THREE of the following statements about different costing systems are correct?

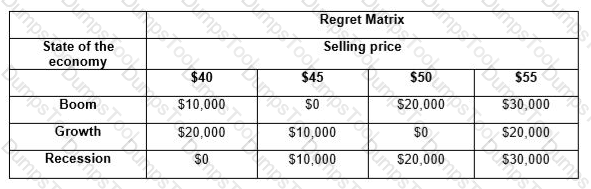

A marketing manager is trying to decide which of four potential selling prices to charge for a new product. The state of the economy is uncertain and may show signs of recession, growth or boom. The manager has prepared a regret matrix showing the regret for each of the possible outcomes depending on the decision made.

If the manager applies the minimax regret criterion to make decisions, which selling price would be chosen?

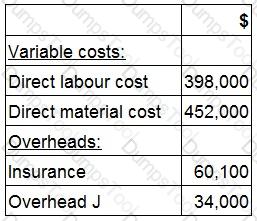

A company's product range includes Product N. The costs relating to Product N are shown below:

The direct labour costs relate to specialists employed to work wholly and exclusively with Product N.

If the company stopped making Product N, the insurance overhead cost would cease, but overhead cost J would be unaffected. Both overheads are absorbed in direct proportion to material costs.

Which of the following costs should be used in the decision whether to stop making Product N?

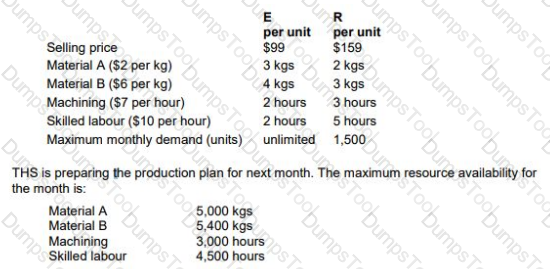

THS produces two products from different combinations of the same resources. Details of the products are shown below:

Identify, using graphical linear programming, the optimal production plan for products E and R to maximize THS’s profit in the month.

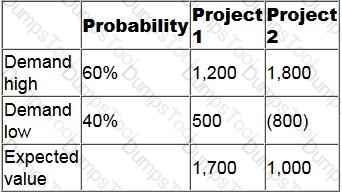

A company is considering two mutually exclusive projects.

The returns on each project, at both high and low demand, have been multipled by the estimated probabilities to calculate the expected values shown in the table below:

Market research would be able to determine with certainty what the level of demand will be.

What is the maximum amount that the company should pay for this certainty?

Company NBO is providing a quote to manufacture 500 passenger seats for a bus company.

Relevant cost is being used as the basis for the quote.

Which THREE of the following should be included as relevant costs or savings in the production of the 500 passenger seats?

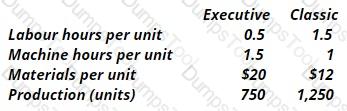

D3 makes 2 types of toilets - the Executive (Ex) and the Classic (CI). Direct labour costs $6 per hr and overheads are absorbed on a machine hour basis. The overhead absorption rate for the period is $28 per machine hour. What is the traditional cost per unit for (Ex) and (CI)?

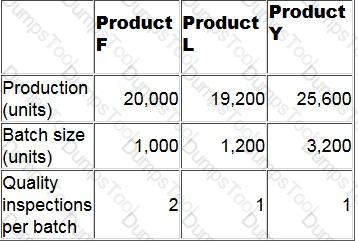

A manufacturing company uses activity-based costing to charge overheads to its three products. One of the main activities is quality inspection. The cost driver is the number of inspections and the budgeted cost is $211,200.

Additional budgeted data.

What is the budgeted quality inspection cost for a unit of product F?

Christian the management accountant at a car manufacturer has been given a list of costs that have been incurred due to accidents and errors either occurring or being prevented.

Which of the following are examples of non-conformance costs? Select ALL that apply.

A company manufactures three products X, Y and Z.

The company is currently operating at full capacity and is unable to meet the full sales demand for Product Z.

According to the latest management accounts, Product Y is loss making, whilst X and Z both make strong positive contributions.

Which of the following is relevant when making a decision on whether or not to discontinue the manufacture of Product Y?

Which THREE of the following are advantages of activity-based costing (ABC), in a multi-product environment, when compared with traditional absorption costing?

A company is preparing its annual budget and is estimating the number of units of Product A that it will sell in each quarter of year 2. Past experience has shown that the trend for sales of the product is represented by the following relationship:

y = a + bx where

y = number of sales units in the quarter a = 10,000 units b = 3,000 units x = the quarter number where 1 = quarter 1 of year 1

Actual sales of Product A in Year 1 were affected by seasonal variations and were as follows:

Quarter 1:14,000 units Quarter2: 18,000 units Quarter 3: 18,000 units Quarter 4: 20,000 units

Calculate the expected sales of Product A (in units) for each quarter of year 2, after adjusting for seasonal variations using the additive model.

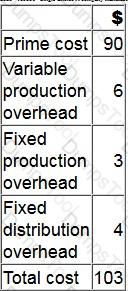

A company manufactures a single product. The cost card for a unit of this product is as follows:

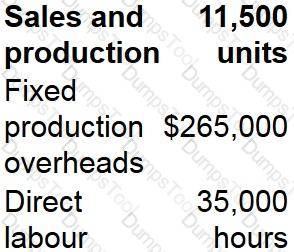

During month 6, finished goods inventory increased by 350 units.

By how much would the profit differ in month 6 if finished goods inventory was valued at standard marginal cost rather than standard absorption cost?

The standard production cost of making a product is as follows:

What is the fixed production overhead capacity variance?

Which of the following statements about total quality management are incorrect? Select ALL that apply.

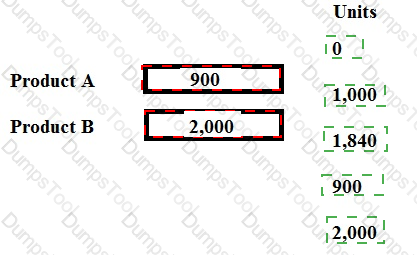

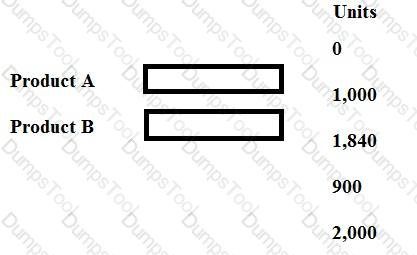

Demand for two products, A and B is 1,000 units and 2,000 units respectively. Each unit of Product A requires 8 kg of material and each unit of Product B requires 5 kg of material. The maximum availability of material is 17,200 kg. Contribution per unit of A is $10 and per unit of B is $9.

Place the production volumes of Product A and Product B, that will maximize contribution, in the table.

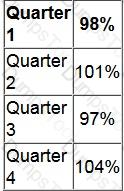

An analysis of past sales data shows that the underlying trend in a company's sales volume can be represented by:

Y = 50X + 625

Where Y is the trend sales units for a quarter and X is the quarterly period number.

The seasonal variation index values have been identified as follows:

The forecast sales volume in units for quarter 4 next year, which is period 14, is:

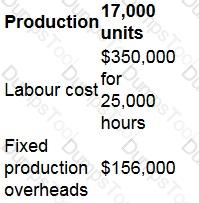

Budgeted sales and production for Product X for this period are 12,000 units.

The standard cost and selling price for a single unit of the product are:

The fixed production overhead expenditure variance is:

A company is basing its budget on predicted sales of one of its products. They have tasked you with forecasting the sales in year 2. The company has found that a fairly accurate prediction can be found when the trend

is calculated like so:

a = 10,000

b = 2,000

The sales of year 1 were affected by seasonal variation and were as follows:

Q1:12,500

Q2:14,200

Q3:15,400

Q4:19,650

You use a multiplicative model and round percentages to the nearest whole percent.

Select ALL the correct quarterly forecasts of year 2 from the list.

Assume that you have made profit calculations based on standard profit calculation methods and activity based costing methods.

In which ways will this information be beneficial to the management team?

Select all the true statements.

Which THREE of the following statements relating to fixed overhead variances are correct?

A company sells and services photocopying machines. Its sales department sells the machines and consumables, including ink and paper, and its service department provides an after sales service to its customers. The after sales service includes planned maintenance of the machine and repairs in the event of a machine breakdown. Service department customers are charged an amount per copy that differs depending on the size of the machine.

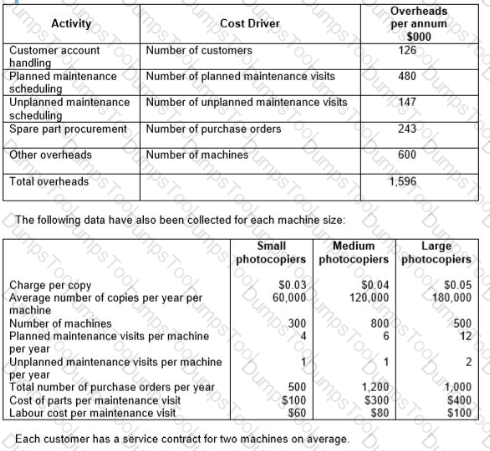

The company’s existing costing system uses a single overhead rate, based on total sales revenue from copy charges, to charge the cost of the Service Department’s support activities to each size of machine. The Service Manager has suggested that the copy charge should more accurately reflect the costs involved. The company’s accountant has decided to implement an activity-based costing system and has obtained the following information about the support activities of the service department:

Calculate the annual profit per machine for each of the three sizes of machine using activity-based costing.

TESTED 28 Jun 2026