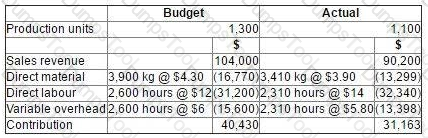

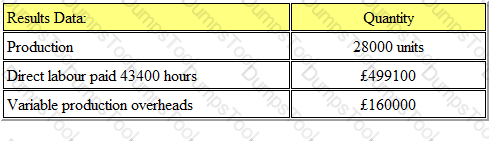

Data for the latest period for a company which makes and sells a single product are as follows:

There were no budgeted or actual changes in inventories during the period.

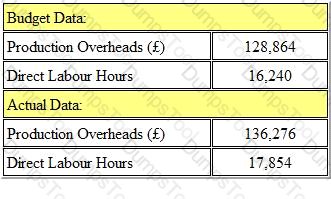

The variable overhead expenditure variance for the period was:

A company uses standard absorption costing. Budgeted and actual data for the latest period are as follows.

What was the production overhead absorption rate per unit?

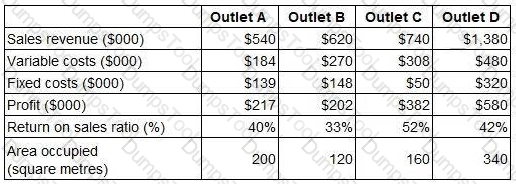

A small airport’s management accountant has prepared the following management report on the performance of its four retail outlets.

Which retail outlet has the highest contribution per square metre?

Which of the following cannot be used to split costs into fixed and variable elements?

Refer to the exhibit.

The following data relates to Department A within a business unit.

The overhead absorption rate per direct labour hour for Department A is:

Give your answer to 2 decimal places.

Within a relevant range of output, the fixed cost per unit of a product will:

Refer to the exhibit.

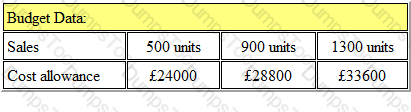

Budget information for 'Crome Ltd' is as follows:

The budgeted cost allowance for the sale of 1000 units would be:

Apex Plc has budgeted to sell 8,000 units of A in the year. Opening inventory of A is estimated at 1,000 units and the company plans to reduce inventory levels of all products by 15%.

What will be the production budget (in units) for the year?

Refer to the Exhibit.

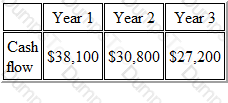

The following forecast cash flows relate to a proposed investment in new delivery vehicles at a total cost of $75,000.

The internal rate of return (IRR) of the proposed investment is (to two decimal places)

Refer to the Exhibit.

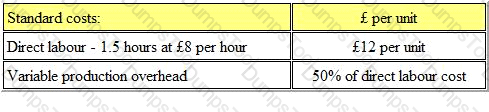

AM Ltd. makes and sells a single product for which the standard cost information is as follows:

What is the variable overhead expenditure variance?

The management accountant has completed the appraisal of an investment in new office equipment.

It has now been discovered that the cost of capital used in the appraisal should have been higher.

What will be the effect on the calculated net present value (NPV) and the payback period?

The standard labour cost for 1 component is $15.00 (5 hours at $3 per hour). Last month, 6,000 hours were worked at a cost of $17,000 to produce 1,100 components. The labour efficiency variance was:

The following costs are incurred by a company which owns a five star hotel. Which THREE of the items would normally be classified as variable costs?

Within a relevant range of output, the variable cost per unit of output will:

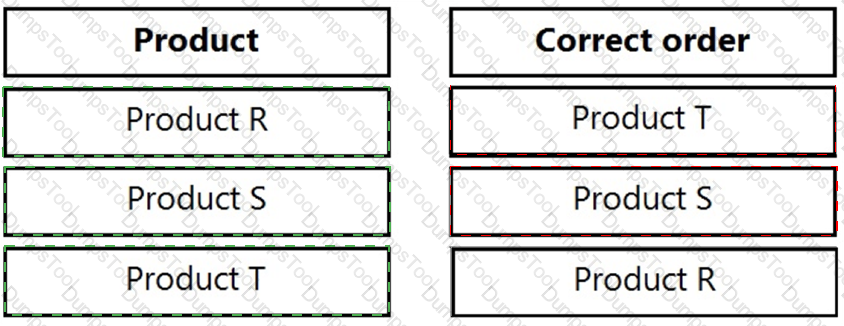

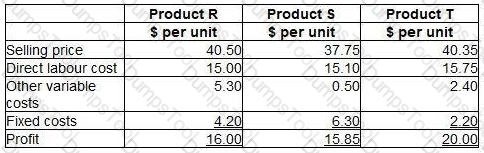

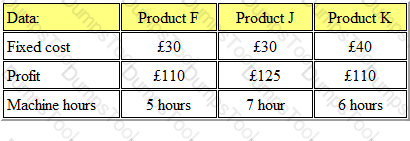

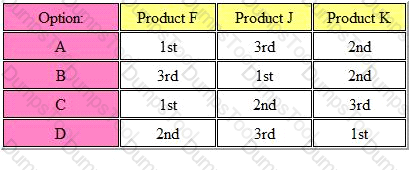

A company manufactures three products using the same direct labour which will be in short supply next month. No inventories are held. Data for the three products are as follows:

The fixed costs are all committed costs and cannot now be altered for the next month.

Place the labels against the correct product to indicate the order of priority for manufacture that will maximise the profit for the next month.

How does Beyond budgeting help to resolve the weaknesses of traditional budgeting? (Select ALL that apply.)

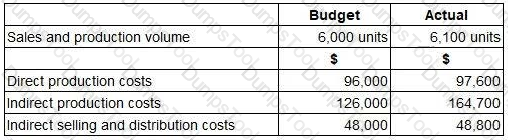

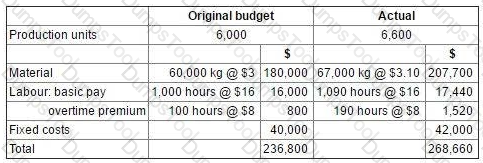

The budget and actual cost statements for the production department for the latest period were as follows.

Notes.

The 10% increase in production was required to meet unexpected additional sales demand.

The production manager is responsible for negotiating the price of materials with suppliers.

The normal working time is 900 hours per period. Any overtime worked above these 900 hours is paid at a premium of 50%.

In preparing the flexible budget for the latest period, which TWO of the following statements are correct? (Choose two.)

Refer to the Exhibit.

Zepher Ltd. manufactures three products, which require the same type of machine. The following fixed cost and profit per unit is available:

In a period in which machine hours are in short supply, which of the following options is the rank order of production?

Answer is:

Refer to the exhibit.

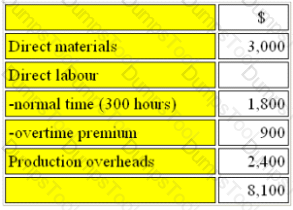

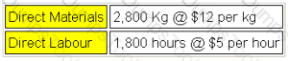

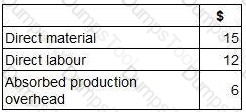

Patchit Limited operates a job costing system. They have been asked to quote for a rush job that will require to be done in overtime hours. It is estimated that the job will incur the following costs:

Production overheads are absorbed on a direct labour hour basis. Budgeted direct labour hours for the year were 50,000 and budgeted direct labour cost was $300,000.

If production overheads had been based on a percentage of direct labour cost, the revised production costs for the job would be:

A company’s cash budgetary plans show that there will be surplus cash for three months of the forthcoming year.

Which THREE of the following would be appropriate management actions in this situation?

Refer to the exhibit.

Which type of cost do the following figures represent?

Refer to the exhibit.

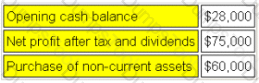

An extract from the budget for GS is given below:

What is the company's budgeted cash holding at the end of the year?

When preparing the material purchases budget, the quantity to be purchased equals:

The variable cost of a product is £7 per unit. The fixed costs of the product are £140,000. The break-even point is 70,000 units.

The selling price of the product is:

Give your answer to 2 decimal places.

In an integrated cost and financial accounting system, the accounting entries for the purchase of raw material on credit would be:

Which ONE of the following would be classified as an internal environmental cost?

Refer to the exhibit.

Xell Ltd uses a standard costing system and therefore values all inventory at standard cost. During period 3 the price paid for material 'A' was £6 per kg less than the standard price.

The following information for material 'A' relates to period 3:

What was the material price variance for period 3?

Refer to the exhibit.

T operates a process costing system. Data is available for Process A for the month of July.

Inputs for the month:

Normal losses are 15% of input and can be sold for $6 per kg. Actual output was 2,600 kg. There is no opening or closing work in progress for the period.

What is the value of the output from the process in the month?

Which of the following statements is correct?

i. sector bodies use budgetary planning and control systems

ii. costing cannot be used by public sector bodies because they have no measurable output

iii. in public sector bodies tend to focus on cost management therefore they have no need for non-financial information

In order to provide information that is suitable for control purposes, the budget must be:

In order for the information in a management accounting report to be authoritative its contents must be:

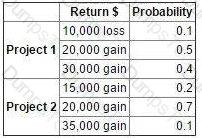

The possible returns and associated probabilities of two independent projects are as follows:

It has been decided that both projects are to be launched.

Which TWO of the following statements are correct? (Choose two.)

Refer to the exhibit.

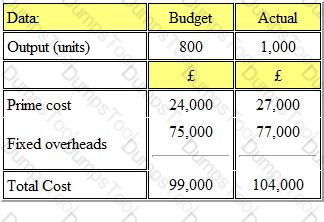

A company issued its production budget based on an anticipated output of 800 units. Actual output was 1000 units. The details of the costs are shown below:

The budget expenditure variance was:

Overtime worked as a result of a rush order at the customers request should be classified as a:

A company's output level increases but remains within the relevant range. Which ONE of the following statements is incorrect?

A company is considering investing $57,000 in a machine that will last for five years, after which time it will have no value. The machine will generate additional revenue of $190,000 each year. Annual running costs, including depreciation of $11,400 will amount to $168,400.

Assuming that all cash flows occur evenly, the payback period of the investment in the machine is closest to:

Which of the following statements relating to risk and uncertainty is correct?

A new product requires an investment of $200,000 in machinery and working capital. The total sales volume over the product’s life will be 5,000 units. The forecast costs per unit throughout the product’s life are as follows:

The product is required to earn a return on investment of 35%.

What unit selling price needs to be achieved?

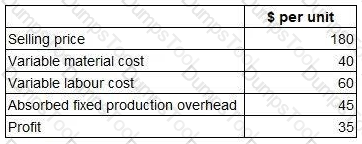

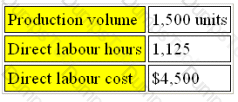

A company makes and sells a range of products. The standard details per unit for one of these products, product X, are as follows.

To meet sales demand, the company must obtain 2,000 units of product X next month. There is sufficient labour capacity to produce 1,500 of these units in-house during normal time. However, any production above this level would require overtime working which would be paid at a premium of 50%.

The company can buy as many units of product X as it wishes next month from an external supplier at a price of $120 per unit.

What is the total financial benefit to the company of purchasing the appropriate number of units from the external supplier rather than producing them in-house?

In a company's sales ledger department, one additional invoice clerk is needed for every eighty customers added to the customer database. The total salary cost of invoice clerks is best described as:

Refer to the exhibit.

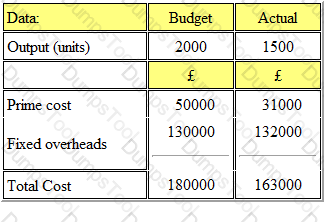

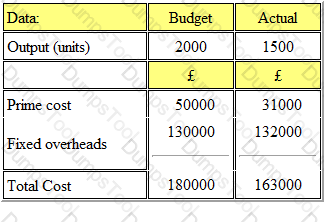

A company issued its production budget based on an anticipated output of 2000 units. The actual output for the period was 1500 units. The details of the costs are shown below:

The budget volume variance was:

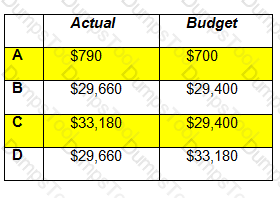

Refer to the exhibit.

A company budgeted to provide 700 units of service last period for a budgeted variable overhead cost of $29,400. During the period a total of 790 units of service were provided and the variable overhead cost incurred was $29,660.

For effective control of variable overhead cost which two figures should be compared in the budgetary control statement?

Refer to the exhibit.

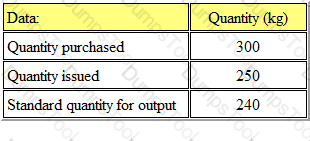

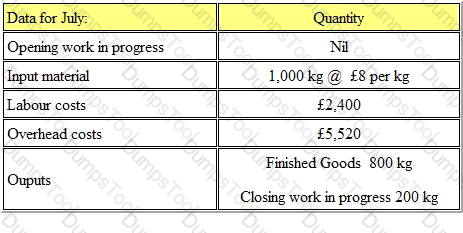

The following data refers to a manufacturing process for the month of July:

The work in progress is completed as follows:

(a) 100% for material

(b) 80% for labour

(c) 60% for overhead

What is the value of the finished goods?

Refer to the exhibit.

The budget for ORG for the month of September contained the following data:

During the month the actual number of units produced was 1,550. The management accounts showed a direct labour rate variance of $200 adverse and direct labour efficiency of $150 adverse.

The actual direct labour cost in the month was:

The following list contains many different types of costs for a business. However, only four of them would be considered costs centres. Which four?

Why is it important to have a professional body such as CIMA in management accounting?

A company provides its managers with monthly budgetary control reports. Which ONE of the following types of financial information is this?

Eton Ltd. operates a manufacturing process that produces product A. Information for this process last month is as follows:

(a) Opening work in progress - 2,500 kg valued at £2,000 for direct material and £1,500 for labour and overheads.

(b) Materials input - 25,000 kg at £2.10 per kg.

(c) Labour - £10,000

(d) Overheads - £5,000

(e) Output during the month - 20,000 kg

(f) There were 7,500 units of closing work in progress which was complete as to materials and 30% complete as to conversion.

(g) Normal loss for the month was 3% of input and all losses have a scrap value of £1 per kg.

What was the value of closing work in progress at the end of the month (to the nearest £)?

Refer to the exhibit.

A company issued its production budget based on an anticipated output of 2000 units. The actual output for the period was 1500 units. The details of the costs are shown below:

What was the budget expenditure variance?

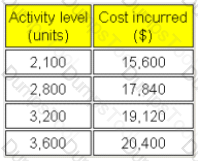

Refer to the exhibit.

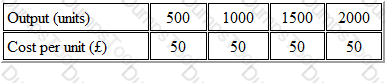

A company has established that a particular cost item is semi-variable. Past records of costs at different levels of activity are as follows:

The fixed cost element for the cost item is:

TESTED 10 Jul 2026